As it stands, the Government has given no indication the furlough scheme will continue beyond October.

The scheme has already been extended twice, once to June, then again into October.

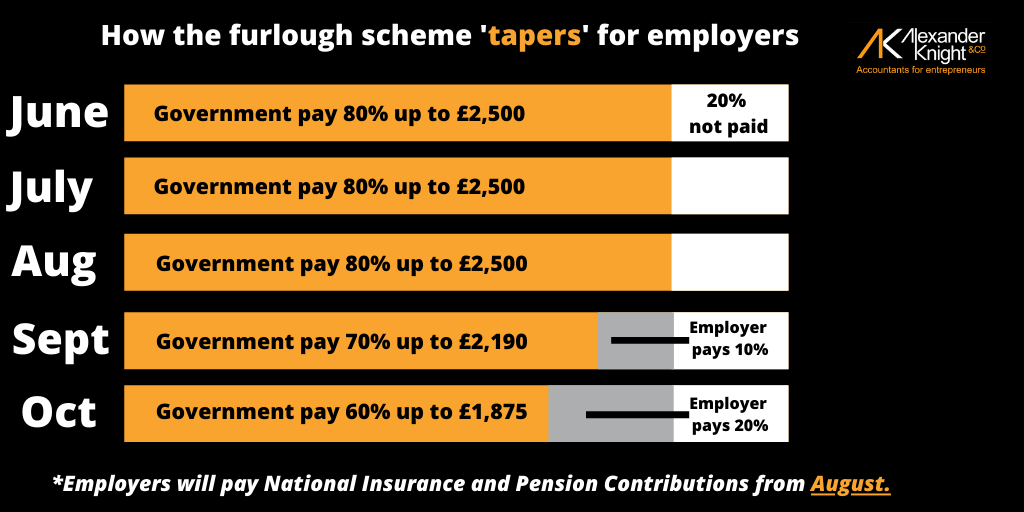

The scheme itself is tapering off and many employers will have important decisions to make on their future staffing needs beyond October.

It is worth a reminder that the Government is launching a job retention bonus of £1,000 (per employee) for employers willing to bring back furloughed employees back into work, in what they hope is an incentive for firms to retain staff beyond January 2021. We don’t yet know how the monies will be claimed but we will inform clients when the details are published.

All our clients who made furlough claims via our team secured the funding on time and we’ve been pleased to help our clients through what can be a complex process of calculation for the uninitiated.

If you need support to review your business plan or staffing levels when the furlough scheme ends then please speak to our team.